- New Customer Inquiries (866) 551-4684

- Customer Service (214) 387-8068

- Make A Payment (866) 558-3328

- Client Portal

- Consumer Support

Missouri’s laws protect lenders and borrowers. Some regulations protect borrowers by restricting the actions of debt collectors, but creditors still have ways to recover debts. Lenders can hire recovery agencies or sue borrowers to enforce the loan agreement or garnish the debtor’s wages to defray the debts. However, deceptive, abusive and unfair debt collection practices are prohibited.

Learn more about Missouri’s collection laws and how a debt recovery service can help.

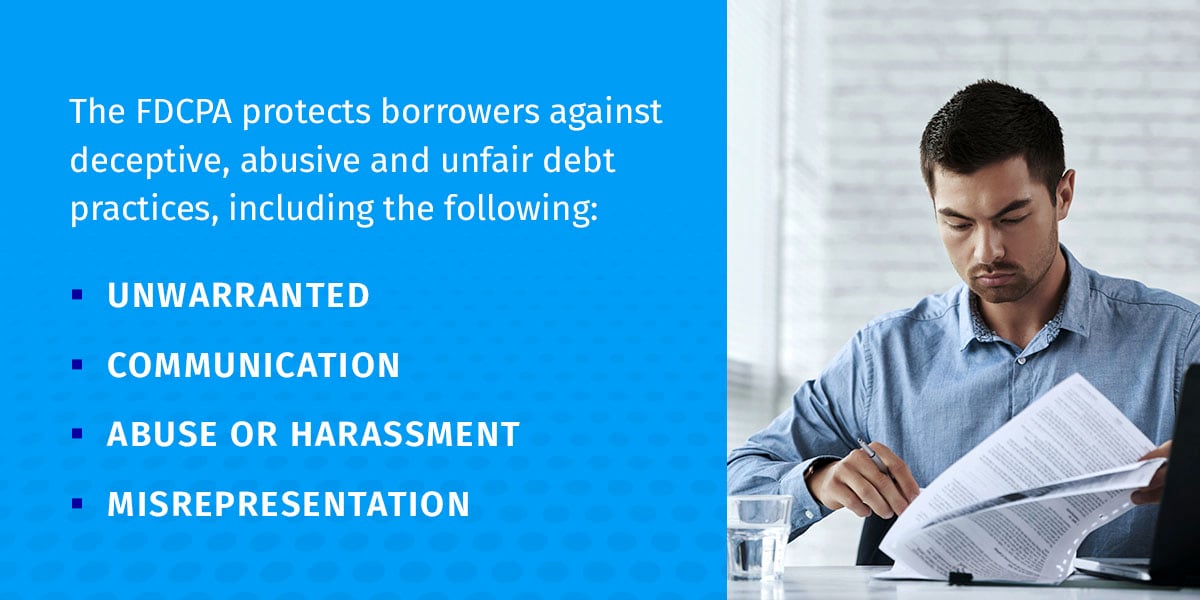

The Fair Debt Collection Practices Act (FDCPA) is a federal law that protects borrowers against deceptive, abusive and unfair debt practices. It restricts debt collectors’ actions, including when and how to communicate with borrowers. The law is applicable in all 50 states.

The FDCPA applies to third-party debt collectors instead of creditors. Additionally, the law excludes business debts — only consumer debts, such as personal, family and household loans, are covered. Credit card debts, personal loans, medical expenses and student loans all qualify as consumer debts.

Federal law defines a debt collector as an individual or business that regularly collects or attempts to collect debt on behalf of another individual or business. A business that collects its own debt in the name of another business may also qualify as a debt collector. Thus, the law applies to third-party debt collectors, debt buyers, debt collection agencies and attorneys acting as debt collectors.

The FDCPA protects borrowers against deceptive, abusive and unfair debt practices, including the following:

Federal law prohibits debt recovery agents from contacting debtors at unusual times and places. An unusual time could be any time between 9 p.m. and 8 a.m. Debt collectors must also avoid contacting debtors at their place of work if the debtors’ employer prohibits such communication. Finally, debt collectors must communicate directly with the debtor’s attorney if they have legal representation, subject to exceptions.

The FDCPA prohibits debt collectors from using profane or obscene language when engaging with borrowers. It also prohibits the debt collector from publishing information about the debtor because they refuse to pay the debt, subject to specified exceptions. Finally, the law protects borrowers from debt collectors who call continuously to annoy, harass or abuse the borrower.

Debt collectors must avoid misrepresenting facts, including the implication of nonpayment of debt, amount and legal status of any debt. Falsely representing to be an attorney is also an FDCPA violation.

Debt collectors who use the threat of force or harm violate the FDCPA. Similarly, threatening to initiate legal action without the legal capacity or intention or to confiscate assets to compel borrowers to pay debt is unlawful.

While the FDCPA prohibits debt collectors from engaging in abusive, deceptive and unfair debt practices, the law allows them to protect their interests in many ways, including the following:

A statute of limitations is a law that provides a timeline within which a party must commence legal proceedings to enforce their rights. Once the time passes, the action becomes statute-barred and the lender loses their right to seek legal remedies in court. It’s like an expiration date for lawsuits.

In Missouri, the limitation period for debts based on written contracts is 10 years. Oral and open-ended debts have a limitation period of five years. The time starts to count when payments are due. If the debtor pays before the expiration date, the time restarts. The debt collector may try to recover the debt without going to court, although the debtor is not obligated to comply.

Debt collectors can declare bad debts and write off loans when deemed unrecoverable. Until then, debtors must repay the loan according to the contract terms. However, borrowers and lenders can negotiate debt settlements if they encounter financial difficulty. Negotiating a debt settlement requires skills acquired through training and years of experience. Follow these tips to increase your chances of success:

Partnering with trusted debt recovery agencies like Southwest Recovery Services, LLC (SWRS) comes with many benefits, including the following:

Here are answers to some common questions:

A debtor can send a letter to a debt collector requesting them to cease all communications. Federal law requires debt collectors to comply with such a request. However, the debt collector may contact the debtor to notify them about the intention to take a specific action, such as commencing legal proceedings.

Generally, debt collectors cannot contact a third party about the debt unless legally required. For example, the debt collectors may hire a third party to discover or verify the debtor’s location. Debt collectors may also contact the debtor’s attorney if they have legal representation.

Debt collectors must identify themselves when they contact debtors and must send a debt validation notice within five days of the first contact to provide details about the debt. The notice must contain information like the creditor’s name, the outstanding amount and how to proceed if the borrower has paid the loan amount with interest in full.

SWRS is a third-party debt recovery agency that provides tailored solutions to lenders nationwide. We have offices in Missouri and many other states, with trained professionals ready to assist. We know how to improve your recovery efforts while complying with the strict legal requirements. To learn more about how we can help you, contact us now!

We make it fast and easy to refer past due and delinquent accounts to our professional recovery agents. You decide the range on what you will accept on each case, and you ONLY pay a percentage of what we actually collect to resolve the case. Ready to get started, or want to learn more? Fill out this form and a dedicate account manager will call you to get started.